2021 Fertiliser Price Hike

Welcome back everyone!

Today on the blog I want to discuss the massive jump in fertiliser prices. Fertilisers provide three main nutrients: nitrogen, phosphorus, and potassium. Nitrogen improves growth, phosphorus stimulates roots and flowering, and potassium strengthens a crops natural resistance. We will explore why 2020-2021 has seen such a huge price increase, as well as the chances of 2022 seeing further price hikes. I’ll be focusing on two of the most widely used products across Australia, urea, and MAP.

UREA

Urea is a soluble organic compound, made up of 46%N (nitrogen). It is the most widely used fertiliser across the globe, largely due to its affordability and the promise of delivering all important nitrogen to the soil. Urea can be dissolved in water prior to application, which is common for those with irrigation. This method is known as ‘fertigation’ and is a fantastic tool to have available in times of drought. The more common method of application is dry spreading; however, this must be done ahead of decent rainfall. Some also choose to direct drill their fertiliser when the timing is appropriate. The concentration of nitrogen in the product can completely impede the germination of seed or give growing plants burns, which is why proper application is so important.

While there is some Urea manufactured in Australia, the high product demand means a majority is imported from the Middle East, China, and Southeast Asia.

MAP

Momo-ammonium phosphate, more commonly referred to as MAP is one of the other most popular fertilisers across Australia. The nitrogen in MAP is in the ammonium form, which resists leaching and is a slower release form of nitrogen. The product has an acid reaction in the soil which can be an advantage in neutral and high pH soils. MAP is spread in the same way as Urea. However the ammonium content of MAP can release toxic gases if stored incorrectly, therefore caution should be taken when handling the product. While part of Australia’s supply of ammonium phosphate fertilisers is manufactured locally, a large portion is imported from Russia and Morocco. A massive 81% was imported in the 2019 financial year; something that will have to change going forward.

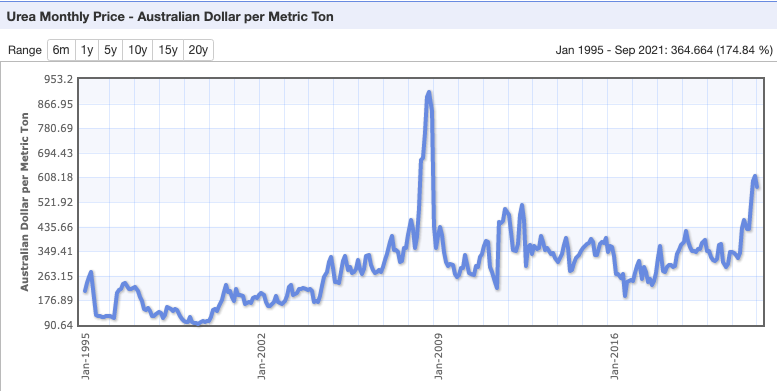

A little bit of history on Australia’s fertiliser prices- many of you will remember the huge jump in prices in 2008. High oil prices and the United States’ rush to biofuel their crops lead to a global fertiliser crisis. The average price of Urea was up to AUD$907 in September 2008. However, the financial crash that soon followed saw a sharp decrease in prices, down to AUD$258 in October of 2009. Since then, the prices have only shifted slightly, remaining around the AUD$400 mark.

What does all that mean for now though? What is causing the 2021 fertiliser shortage? China’s National Development and Reform Commission (NDRC) are looking to restrict the production and export of phosphorus. This is for two reasons: they want to ensure their farmers are cared for first, and they want to lower their emissions. 65% of Australia’s MAP is sourced from China, which puts far more strain on all other countries who manufacture the product as well. This pause on export is expected to remain in place until mid 2022 at the earliest. A mixture of high gas prices, wild weather and unexpected plant shutdowns across the globe has also made nitrate a scarce resource. Thankfully, areas in Queensland, the Northern Territory and Western Australia are capable of producing phosphorus and nitrate, but not enough to meet demand.

As a result, the current price of urea is well in excess of $700/t in most areas. MAP is also seeing prices around the $1000/t mark for Central and Western NSW. These prices are to remain high until the supply chain can catch up, hopefully in 2023.

The ability to bulk buy fertiliser drastically reduces the cost. Bulk purchasing can avoid the use of bags, which is also a far safer method as product handling is minimised. Many who rely on the product have already bought their fertiliser, storing it in their silos until next season in a bid to avoid further price increases. With adequate storage, many of our customers will save thousands if the prices continue to rise, as they are expected to. We see the same market patterns with grain sales, each time those with proper storage readily available, get the upper hand.

HE Silos design and manufacture a range of fertiliser silos from 36m3 to 90m3, however their team of engineers are always eager to cater to whatever your needs may be. A 2-part epoxy coating is applied to protect against even the most corrosive of fertilisers. Use of specialised products can and will save you money by giving you relief in times of price surges, not the mention fertiliser that if stored correctly, won’t be damaged by moisture.

I’m intrigued to see where this spike in pricing ends. If judging by the global economic situation, prices may never return to where they were, only 2 short years ago.

Steve, The Silologist

SOURCES

https://www.indexmundi.com/commodities/?commodity=urea&months=240¤cy=aud