Grain Markets

Welcome back for yet another instalment of The Silologist™.

Today I want to discuss the ever-changing grain markets and have a look into the variables affecting your return on investment.

Wheat is still the dominant grain produced in Australia, with barley and canola our other two industry leaders. As you all know, the grain markets fluctuate day-by-day, particularly around harvest. Historically, Australian markets have taken huge hits as a result of trade disputes, weather patterns and of course, resource availability. The markets will be worth monitoring over the next 24 months as input costs skyrocket across the country due to phosphate shortages (Fertiliser prices have actually reduced but fuel/oil have risen).

WHEAT

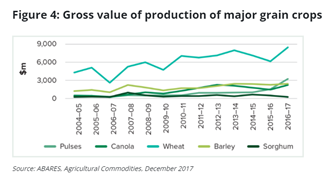

The Australian Bureau of Agriculture and Resource Economics and Sciences (ABARES) data reports that from the 2013-14 to 2017-18 seasons, an average of 12.3 million hectares was planted per annum, with an average production of 24.3 million tonnes with a value of $7.1 billion Australian dollars. Since 2018, Australian wheat prices have sat between and average of $200-$300 tonne for APH standards. May 2005 and October 2016 have seen some of the lowest dollar per tonne figures over the last 20 years at around $150.

BARLEY

The highest per tonne amount for barley over the last 20 years was an average of $257 back in July 2008, however recent average contract prices have been on the increase as well, with many getting around the $250 mark. Thankfully, barley is a far tougher cereal that can withstand much harsher conditions, which is why less was sown over the last few seasons with growers capitalising on wet weather. From 2013–14 to 2017–18, an average of 3.9 million hectares of barley was planted per annum, resulting in average annual production of 9.6 million tonnes with a gross value of $2.3 billion. Barley is one of the most sought-after export commodities, with 30-40% of the global surplus malting barley, and approx. 20% of the global feed market.

CANOLA

An average of 2.5 million hectares of canola was planted per annum, resulting in annual average production of 3.4 million tonnes with a value of $1.68 billion between 2013-14 and 2017-18. In regard to exports, Europe continues to show major increase in the purchasing of Australian canola and they seek to increase their biofuel production. 2020 and 2021 were big years for canola as many growers wanted to make the most of high value and the higher than average rainfall. Coming into the 2022 season, many people are missing out on first generation canola seed as the demand skyrockets.

VARIABLES

Return on investment (ROI) is always a big talking point amongst growers. You can make $500k on a paddock, but if you spent $450k on seed, fertiliser, contractors and marketing, its not the best investment. Obviously, the variables in cropping are huge. Some people sow just enough to feed their stock and hope for the best. While others will meticulously plan their seasons years in advance, knowing exactly what seed will go in what paddock, with rotations, soil testing and advanced screening processes.

CALCULATING RETURN ON INVESTMENT (ROI)

NET PROFIT ÷ COST OF INVESTMENT × 100 = %ROI

There are of course factors that cant be controlled, weather being the biggest one. So it really is impossible to make a judgement on ROI ahead of time, but having a goal is good. Something always worth doing to help your ROI is watching the markets, both sale prices and input prices. Sale prices do have trends, typical times where prices drop, and other times where prices rise. Historically, dollar per tonne value will drop around January-March, with August usually being the month in which the highest contract prices are reported. This is one of the biggest reasons people choose on-farm storage. Most bulk grain storage facilities will start charging costs of storage/carry costs on your grain either immediately, or after a few months, which often pushes people to sell when prices are at their lowest. On-farm storage allows for growers to watch the markets and sell when they are ready and satisfied with the price. Another benefit of on-farm storage is being able to avoid sowing mark ups for seed and use what they have grown themselves.

Input costs are a big talking point coming into 2022. Canola seed prices are a reflection of the increased demand, which hasn’t stopped many people as the market for canola shows no signs of cooling down any time soon. Fertiliser is most likely to be the first thing cut off for many growers as they try to retain their ROI. A phosphate import shortage has caused prices for urea, MAP and DAP to explode over the last 12 months, with prices set to remain high throughout 2022 and into 2023.

Many growers are looking to incorporate pulse and legumins into their sowing rotation to look at improving nitrogen in their soils organically and finding the right match for your system is key. Utilising soil test data and planning are still the most cost effective ways of determining profitable rates for paddocks.

There’s a lot to watch out for as 2022 kicks off. It’s important to keep a keen eye on the price trends and really consider the pros and cons of your chosen inputs. A good return is always the goal, but sometimes things just don’t go to plan. Have a plan, be prepared.

Steve, The Silologist™